Bonus Material: Get the free wealth snowball calculator to tell you how many assets you need to acquire and how long it will take you to be financially free

This strategy isn’t ideal for everyone.

It’s designed for people who want to be in financially free and are interested in systematically acquiring assets that produce cashflow on a consistent and scalable basis and are tired of the wall street circus show with stocks and mutual funds going up and down like a roller coaster. A system that will help you be financially free in 10 years or less even though I started it in my 40s.

In fact, it’s the same financial strategy I’m personally using and other people in the financial industry have advocated for decades, including people like Robert Kiyosaki in “Rich Dad Poor Dad”, Robert Allen in his book “Creating Wealth”, and my own personal mentors at Cashflow Tactics who first introduced me to the concept.

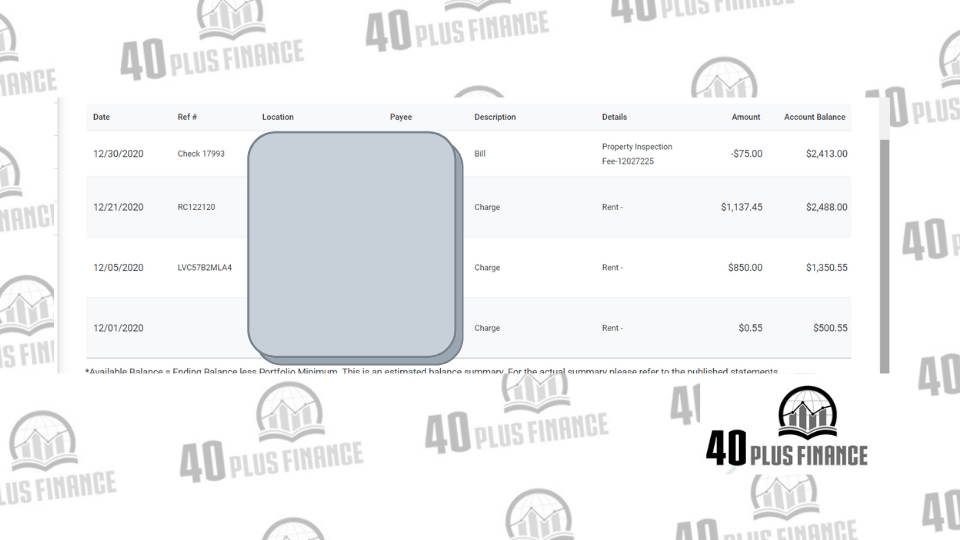

It’s the strategy I’m personally using to passively buy assets that put money in my pocket consistently month after month without sacrificing my dreams of spending more time with my family and feeling like I’m taking on a 2nd or third job at the same time (see snapshot below from a financial portal I use to help manage this strategy)

If you want to be financially free and leave behind the chaos of wall street and follow a stable, predictable, time tested strategy, then this strategy is for you.

Grab my software below to see how many real estate assets you would need in order to be financially free and how long it will take below:

Access The Wealth Snowball Calculator Here

If you are, like I was, without a solid plan for financial freedom and don’t really understand when your current financial plan will let you retire, I recommend you read this first: Use the financial freedom calculator

The Wealth Snowball Strategy: The Three Steps to Achieving Financial Freedom In Your 40s

Stocks, index funds and 401ks are all what most people focus on for long term financial growth. But nothing beats a financial system utilizing simple real estate with compounding returns, that delivers consistent cashflow month after month.

Here’s what a strategy focused on cashflow from real estate looks like:

Ask any investor who has been around a while what their financial strategy is for retirement is, and they will tell you this:

-

Go to school

-

Work hard, & get a steady job

-

Save 10% of your paycheck

-

Watch as your retirement nest egg grew at 8% per year and wait 40 years to retire

Who hasn’t heard that before?

After the “Great Recession” in 2008 it was particularly hard as my family had little to no savings left after pulling ourselves out of it. And, now, during the “Great Shutdown” I’m hearing oddly similar conversations to what I had before. Some of my friends are upset and quite frankly scared about their future and fear they will never be able to retire.

Especially with the stock market bouncing around like it has. Who knows what it will be like when you need to retire (or are told you need to)?

Frig that….way too unpredictable for me. I want a system that I can just follow over and over that doesn’t take constant monitoring and work on a daily or weekly basis.

Quite frankly, that is why I am writing today to let you know about a financial strategy and system that I adopted about two years ago. It sheltered me from losing a dime during the Spring of 2020 and gave me such certainty in my financial plan that I doubled down on it in April of 2020.

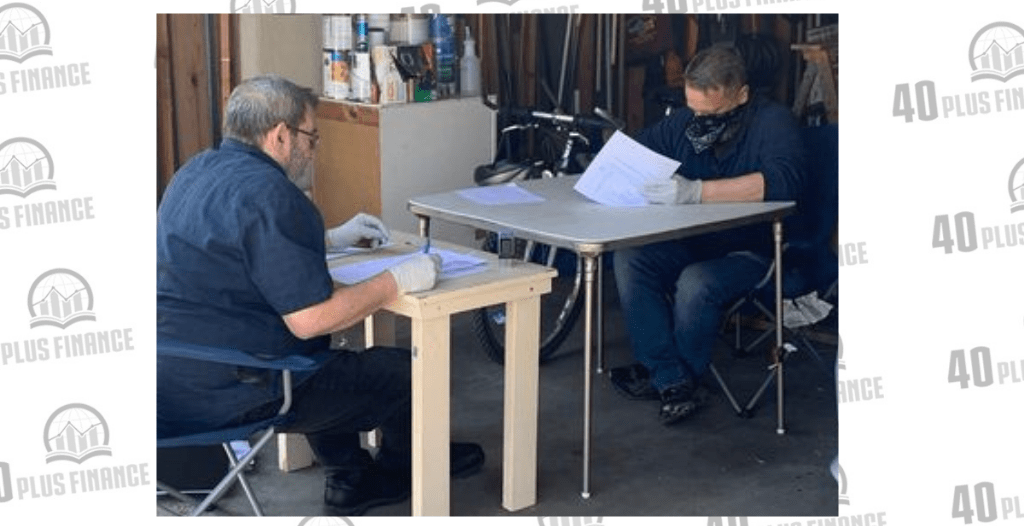

I used the wealth snowball strategy to purchase an asset that paid me $850 dollars a month right in the middle of the pandemic in April 2020.

Here is a picture of me closing on the purchase of an asset as part of that system right in the middle of the worst part of the pandemic, April 2020. I’m the guy with the bandana on :)

But, I didn’t just follow a willy-nilly plan and randomly purchase real estate. I followed a systematic plan that is time tested and repeatable. It gave me the confidence to keep following it’s path even during some of the worst financial times in the last decade.

What did I do?

The Three Steps to Using the “Wealth Snowball” To Achieving Financial Freedom In 10 Years Or Less

There are really only three steps to executing this strategy

-

Determine that your “financial freedom number” is

-

Figure out how many real estate assets you need to meet your number

-

Purchase your 1st cashflowing asset and repeat #3 until you have enough assets.

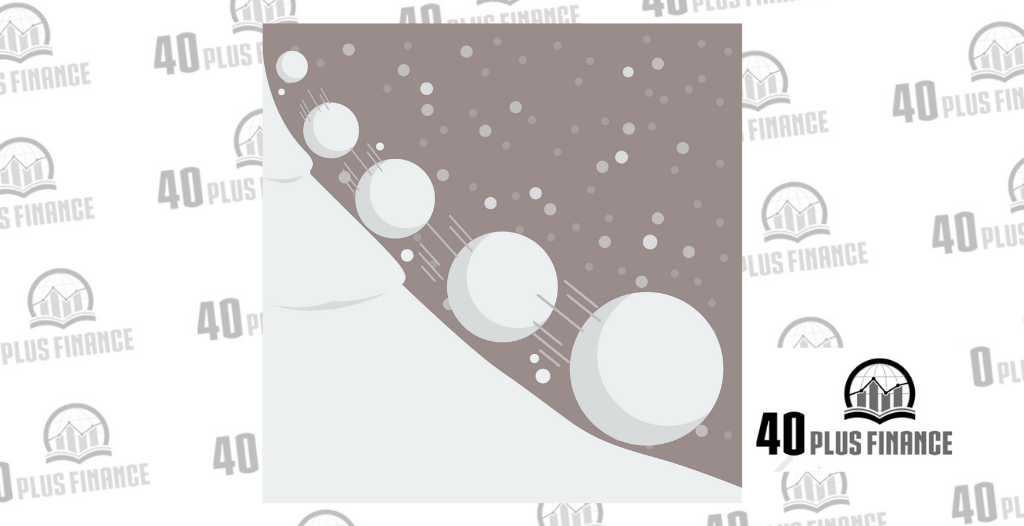

Below is a breakdown of how every part of the strategy works. But first let me tell you what this has to do with a snowball. Have you ever rolled a snowball and seen it get bigger and bigger with each roll? What about a snowball rolling downhill?

Once it gets to a certain size, it starts to momentum and can roll on its own, just like the image below:

The same holds true for wealth. Once you start generating cashflow (which we will talk about below) from one asset and you contribute that to the purchase of the 2nd asset.

And then once you get your 2nd asset and use the cashflow from BOTH of the assets to contribute to your THIRD asset. You start to gain momentum and your “little snowball of wealth” grows and grows with the purchase of each subsequent asset. And so on and you just keep repeating the process

Bonus: I put together a little piece of software which will tell you how many assets you need in order to become financially free using this exact system. Get It Here

By the time you have completed your plan, you are producing enough cashflow from all of your real estate assets that your cashflow exceeds expenses. Here is the entire goal:

Financial Freedom = Cashflow > Expenses

Step 1: Determine that your “financial freedom number” is

This is a pretty simple math exercise here. Remember, our goal is to produce enough cashflow from real estate in order to meet all of our expenses. That will make you financially free.

So how do you determine this? Or more importantly, what is financial freedom for you individually?

For our definition, first add up all of your monthly expenses. Things like: groceries, mortgage, car payments, etc. Everything you need to live comfortably but not things like taxes, savings and such.

This isn’t an exercise of what you’d “prefer” your life to be like and what the expenses are right now, rather where you are now and what you’d need to live off of.

This isn’t an Income number, but rather an expenses number. No need to calculate taxes here. For example, when I went through this exercise the first time, I calculated that my expenses were $5500/month.

THAT is your financial freedom number.

This is the whole goal in what it boils down to

Financial Freedom = Cashflow > Expenses

Want to see what your own wealth snowball looks like? I put together a free calculator which will tell you how many assets you need to meet your financial freedom number and how long it will take. Access The Wealth Snowball Calculator Here

Step 2: Figure out how many real estate assets you need to meet your number

This really boils down to how many pieces of real estate do I need in order to be financially free and how long will it take me?

In order to solve for this problem, one needs to do two things:

- Figure out how many cashflowing assets one needs to accumulate in order for your total cashflow to equal expenses

- Figure out how long it will take you to do so

First, lets solve for how many assets one needs to accumulate. Simple math here will give us an answer:

Monthly Expenses / Cashflow per Asset = # of assets

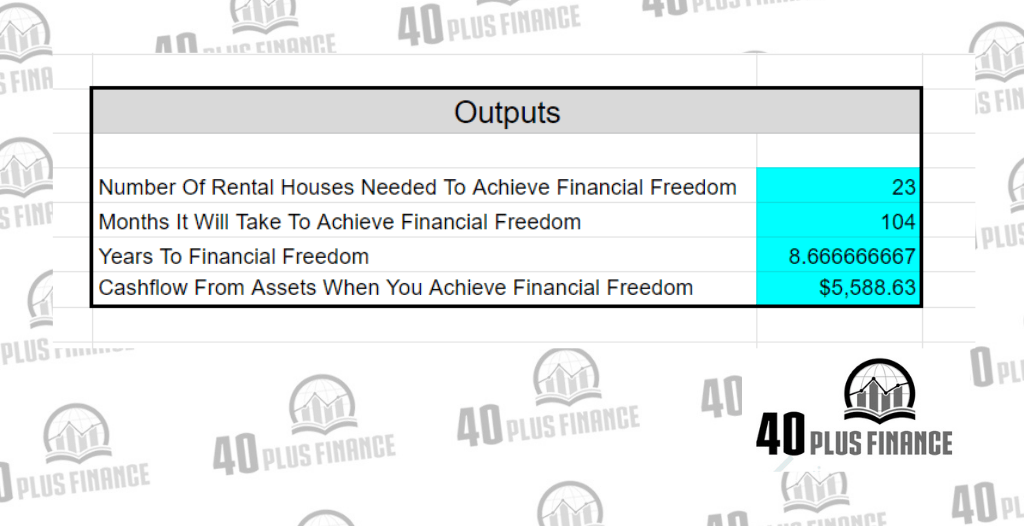

In my case this equals 5500/$243 = 23 assets I need to purchase in order to accomplish this. On first glance this seems like alot, but remember the second part of the formula, how long will it take for me to get there?

Here is where the magic of the wealth snowball comes into play and why I recommend real estate as THE path for achieving financial freedom. It really boils down to how quickly one can accumulate enough capital (cash) for down payments for those 23 rental properties.

So there are three parts to this:

-

How much I have to invest to start out with

-

How much I can contribute each month

-

How to leverage the assets we are purchasing in order to help us along

The first part is pretty simple, and in my case, I am able to contribute $2k/month in savings to this plan. Plus, I was able to contribute roughly $45,000 in cash to the entire plan to get it kick started (more on this in another post).

Now, before we go any further, let me state this. At this point I already have 6 months of emergency savings stored up and I have eliminated most consumer debt, with the exception of car payments and a payment on my primary residence.

If you aren’t at this point yet, I recommend getting to this point ASAP before proceeding any further.

Here is the beauty of focusing on acquiring cashflowing assets. You add the cashflow from those rentals to how much you are able to invest each month towards your financial freedom plan.

Let’s use me as an example here. Before I acquired asset #1, I was able to contribute $2000/month towards my goal of achieving financial freedom in 10 years.

After purchasing asset #1, I was able to contribute the $2000 PLUS $243 for a total of $2243/month.

After purchasing asset #2, I was able to contribute the $2000 PLUS ($243 x 2) for a total of $2486/month.

And so on. I refer to this method as the wealth snowball where you are continually rolling cashflow into your financial freedom plan in order to get you to achieve financial freedom in 10 years. By continually rolling the cashflow accumulated from your assets into your financial freedom plan, you accelerate the rate at which you save up cash much like how a snowball rolling down hill accelerates with the more snow it pulls into the snowball.

So, does the math work out for me to achieve this in 10 years? As it turn out, yes, looking at the image below, I will be able to achieve it in 8.6 years.

Want to see how many assets you need and how long it will take to acquire them? Access The Wealth Snowball Calculator Here

Now let me say that no plan will go exactly as you predict for 10 years. Circumstances change, the economy changes, and goals change. But the plan gets you headed in the right direction and gives you time based goals to work towards.

Step 3: Purchase your 1st cashflowing asset and wash rinse repeat until you have the number you determined in #2

Ok, so now that we have a plan, how do you know what kind of real estate to purchase? Do you go out, hunt for bargain real estate and start renovating them?

Heck no.

Here is what one auto pilot asset looks like and how much cashflow it can kick off on a monthly basis.

Real Estate is the solution I came up with, but remember, we don’t want to spend a ton of time on real estate and we are going to get into and execute real estate in such a way that it requires a minimal amount of time.

Remember the simple, repeatable system here that I mentioned before that you can do over and over again and that will get us to our goal of financial freedom in 10 years or less?

We are going to “do” real estate in a very specific way, popularly known as Turnkey Real Estate Investing.

What is Turnkey real estate investing?

Simply put, it’s where you work with a third party company that does the following for you (and I emphasize for you)

-

Find the best properties

-

Rehab the properties

-

Sell the property to you (the investor)

-

Find a suitable tenant for you

-

Manage the property on your behalf

You simply supply a down payment for purchases of the property. Hence the name “Turnkey”.

Listen, there are a TON of ways to “do” real estate, but none of them fit all of the criteria I’d outlined above. This particular real estate strategy isn’t necessarily focused on getting the largest ROI, but rather it’s centered around taking advantage of the cashflow from these properties, getting the tax advantages, and requiring a minimal amount of time on a monthly basis.

So we are going to create a system for ourselves that requires the minimum amount of time, yet still achieves our goal of achieving financial freedom in 10 years or less. Ok, so lets roll through the numbers here, what does one simple real estate asset look like and how much cashflow could it kick off?

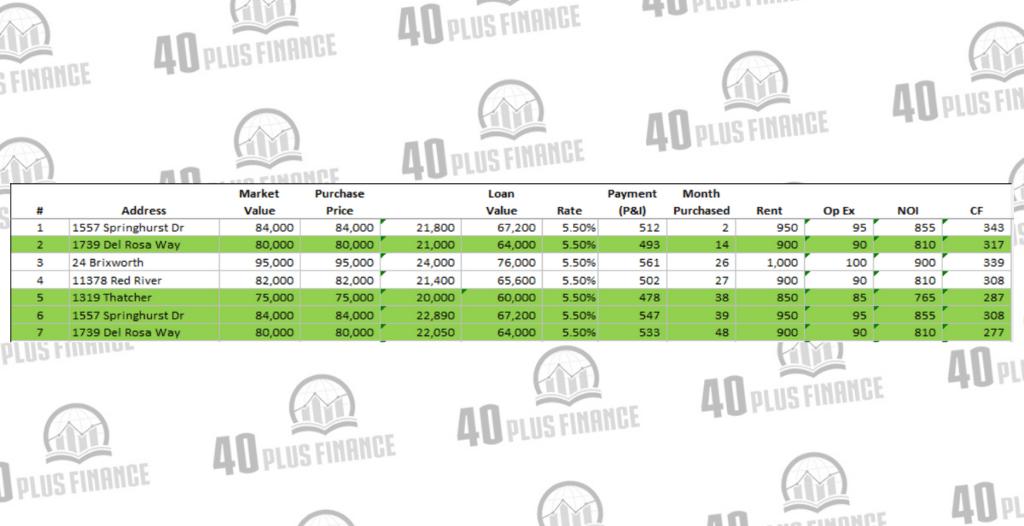

For the markets I am looking for, typically an asset will look something like the ones listed in the spreadsheet below:

Here is a quick breakdown of column headers:

- Market Value - The current market value of the property

- Purchase Price - Generally the same as the market value

- Loan Value - How much of a loan you will need to take out in order to acquire the asset (more on this later)

- Monthly payment - How much the payment will need to be in order to service the loan at any given amount.

- Rent - The amount someone who rents the property will pay

- Op Ex - Operating Expenses. These are known expenses (such a taxes) that you’ll have to pay on a monthly basis.

- NOI - Net Operating Income -NOI equals all revenue from the property, minus all reasonably necessary operating expenses

- Cashflow - In this case is equal to NOI minus the monthly payment

One value that did not have a heading was the down payment on the property, which in the case of the top image, how much capital would be required in order to purchase the property.

As you can see from the image above I needed to accumulate enough cashflowing assets in order kick off enough cashflow monthly where my cashflow is greater than expenses.

So what is the wealth snowball system for financial freedom?

Basically you buy one real estate asset, use your own savings plus the cashflow from that first asset to save up enough money to purchase the 2nd asset. Then use the cashflow from the two pieces of real estate to purchase the third and so on.

You keep doing this over and over until you have purchased enough assets for the cashflow to exceed your financial freedom number.

Now You Try It

Along the way, you are going to acquire other skills:

-

How to save your money and store it in a secure place for emergencies

-

How to find and acquire these cashflowing assets

-

How to take advantage of tax strategies

But it all start with a preliminary plan and the vision to see the possibility of a future of financial freedom:

To get started, get the software download where you can see how many little green houses of real estate you’ll need to be financially free: