When people first hear about financial freedom, the first thing that comes to mind is thoughts of luxurious houses, extensive vacations, and smoking cigars in dark rooms where massive deals are being made. What does financial freedom mean to the average person? Financial freedom is a dream many of us share; it means different things to everyone. For some individuals, it might mean traveling the world without worrying about money, while for others, it could mean staying home and caring for a family. At its core, financial freedom is about having enough passive income to live the lifestyle we desire without being tied down by financial constraints. As we navigate the world of personal finance, we need to define what financial freedom means to us individually. By understanding our financial goals and dreams, we can better plan, save, and invest in a way that will help us achieve the freedom we seek. We must move beyond traditional financial advice and explore new ways of investing that align with our unique goals and values. Do we have what it takes to achieve financial freedom? Absolutely. But it requires discipline, patience, and a willingness to embrace change. No matter our age, it’s never too late to begin working toward our financial dreams. Let’s explore the concept of financial freedom together, break free from traditional constraints, and build a financial future that allows us to live life on our terms. Key Takeaways:

- Financial freedom means having enough savings, investments, cash, or cash-flowing assets to live life on your own terms.

- Financial freedom can be formally defined as: Income from “investments” > expenses.

- Your “financial freedom number” is the amount you need to cover your current day-to-day expenses.

- Two general frameworks for achieving financial freedom: 1) Asset accumulation (e.g., FIRE movement or traditional investing) and 2) Cash-flowing assets (e.g., real estate or dividend funds).

- Defining what financial freedom means to you personally is an essential starting point.

- Managing money, becoming conscious of spending habits, and creating a budget are crucial steps to achieving financial freedom.

- Paying off debt and establishing an emergency fund are important components of securing financial freedom.

Understanding Financial Freedom

Defining Financial Freedom

When people first hear about financial freedom, the first thing that comes to mind is thoughts of luxurious houses, extensive vacations, and smoking cigars in dark rooms where massive deals are being made. Generally speaking, it means having enough savings, investments, cash, or cash-flowing assets to live life as you want on your terms. The ability to do what you want, when, and with whom you want to sum it up. To make the definition more formal, let’s put it into a formula. Financial Freedom = income from “investments”> expenses. A vital component of this is what is known as your “financial freedom number.” In the context of the above formula, your “number” is the day-to-day expenses that you need to meet to live life as it is right now. Not some future version of yourself, but rather what it would take to pay our own bills today. You compute this by tallying all of your expenses up monthly, including a mortgage, car expenses, medical expenses, food, etc. Everything you need to live as you do today. For the sake of an example, let’s say that all of your expenses each month were $5,300. All your investments (whether through withdrawals, sales, cash flow, etc.) must equal or exceed that number monthly. When you achieve that, you are, by definition, financially free. Financial freedom is a term that can feel elusive, but at its core, it’s about having control over our finances. It’s the ability to do what we wish without being hampered by debt, constrained by a strict budget, or need to work for every dollar. So, how can we define financial freedom for ourselves? It all starts with understanding our income, savings, and expenses - and taking control of them.

Benefits of Financial Freedom

Why should we strive for financial freedom? Firstly, it gives us the peace of mind to enjoy our lives, knowing that our economic future is secure. Secondly, it allows us to create a lifestyle that aligns with our values and priorities without being dictated to by financial constraints. And finally, by having our money work for us, we can achieve the freedom to retire confidently, knowing that our golden years will be well-funded and stress-free.

The Role of Income and Savings

As we know, the cornerstone of financial freedom lies in our income and savings. But it’s not just about earning and saving more; it’s also about managing our finances wisely. Heeding some habits of financial freedom, we can create a solid budget, reduce debt, and automate savings to have a robust economic foundation. Remember, we don’t need to be wealthy to be financially free - we just need a solid income and savings plan that aligns with our lifestyles and goals. So who’s ready to create that plan and work toward financial freedom? Let’s do it together.

Steps to Achieve Financial Freedom

Generally speaking, people follow two frameworks or paths when working toward financial freedom. We will get into the frameworks in a bit, but first, we must establish what is required to increase your general sense of financial security.

Paying off Debt

Our journey to financial freedom starts with facing our debts. We all have bills, whether credit cards, student loans, or a mortgage. Tackling debt means becoming familiar with our financial obligations and formulating a plan to pay them off. By paying off high-interest debts first, we can save ourselves significant money in the long run. Remember, debt is a constant barrier to achieving financial independence, so the sooner we get rid of it, the better.

Creating and Managing a Budget

A crucial step toward financial freedom is creating and managing a budget. A very clear understanding of our income and expenses allows us to make better financial decisions, reduce frivolous spending, and allocate our resources more effectively. Budgeting helps us prioritize our goals, distinguish between needs and wants, and keep our spending in check. Plus, visualizing our cash flow helps prevent living paycheck to paycheck.

Building an Emergency Fund

Life is full of surprises, sometimes with a hefty price tag. We can’t predict when an emergency will strike, like an unexpected medical bill or a job loss, but we can be prepared for it. Establishing an emergency fund is essential to financial freedom, providing us with a safety net during uncertain times. Experts recommend having at least 3-6 months’ worth of living expenses in an easily accessible savings account. This way, we’ll have the peace of mind that comes with knowing we’re prepared for life’s curveballs.

Investing for Wealth Growth

The first is through an accumulation of assets and wealth growth that, once you have “enough” of them, you can live off of as you draw them down. The rule governing the drawdown of assets is more commonly known as the “4% rule” and means that you shouldn’t withdraw more than 4% of your assets in any given year. People approach this in one of two ways. The FIRE (Financial Independence Retire Early) movement focuses on extreme savings and investing. This often requires saving up to 50% of your income towards that goal to “retire” early. The first step towards FIRE is tracking your spending. You can use a program like Mint or YNAB (or your personal choice) to track your spending and determine where you spend your money. With Mint, you can see which categories you’re overspending and which ones you’re under. You can also set goals using the app and keep yourself accountable. When you’re responsible for your financial future, you’ll be able to enjoy the joy of achieving financial freedom. This was made famous by the blogger Mr. Money Moustache, and we don’t personally adhere to the austerity technique of FIRE; it’s become trendy, particularly among millennials. Next would be a more traditional, accumulation-based approach, saving money in financial investments such as stocks, bonds, mutual funds, etc. You can use our financial freedom calculator to see how on track you are on your path and at what age you should be able to retire.

Generating Passive Income

Lastly, one of the ultimate goals in achieving financial freedom is generating passive income. Passive income is money earned with little to no effort, which means we’re free to pursue our passions, travel, or simply enjoy life. There are almost an infinite number of ways to create passive income streams, such as real estate investing, dividends from stocks, royalties, or even starting a side business. When our passive income covers all our expenses, we can finally be financially independent. The second overall approach is through buying and holding cash-flowing assets to accumulate enough assets that kick off cash-flow to eventually meet your financial freedom number. Another way to think of this is diversifying your sources of income while utilizing your retirement savings. Two popular investment vehicles for this are either real estate or dividend fund investing. In the example we gave earlier in the article, with a goal of $5300, let’s say you decide on the real estate approach. Using an example of each property kicking off $250 per month in positive cash-flow, it would the final solution would look like this: $5300 / $250 = 21 properties. Once you have purchased all those properties, each kicking off its particular cash flow, you have become financially free.

Maintaining Financial Freedom

Adopting the Right Mindset

One crucial aspect of maintaining financial freedom is adopting the right mindset. We must learn to embrace frugality and resist the temptation to splurge on unnecessary items. Let’s ask ourselves, do we need that daily coffee from the fancy café when we can make it at home? Prioritize saving and investing over unnecessary spending, focusing on our long-term financial goals. Remember, changing our habits and working towards financial freedom is never too late.

Utilizing Budgeting Tools and Resources

As we work on maintaining our financial freedom, we must keep track of our income and expenses diligently. We can access various budgeting tools and resources, including budgeting apps like Mint. We can use these resources to monitor our spending habits and make necessary adjustments. By staying on top of our finances, we ensure we can make informed decisions and plan for future expenses, such as traveling.

Protecting Your Assets

Maintaining financial freedom means taking proper care of our assets, including our credit history and investment accounts. For example, we must consistently review our credit reports, ensuring accuracy and addressing discrepancies. Let’s also diversify our investment portfolio, making sure it aligns with our risk tolerance and financial goals. This way, our assets will continue to work for us, providing a solid financial foundation and a safety net. To reiterate, a critical part of protecting your assets is maintaining the emergency fund we discussed earlier. The more resilient you are in the face of whatever unexpected expenses arise (and they will) without relying on growing your credit card debt, the closer you will be to achieving financial independence.

Estate Planning

Estate planning is an aspect of financial freedom we cannot ignore, especially as we age. Creating a plan for our legacy that includes wills, trusts, and beneficiary designations is essential. Don’t forget to save for our children’s or grandchildren’s education through 529 programs and contribute to retirement accounts where our employer offers a matching contribution. By proactively planning our estate, we ensure our loved ones are taken care of and help solidify our financial freedom.

What Does Financial Freedom Mean To You?

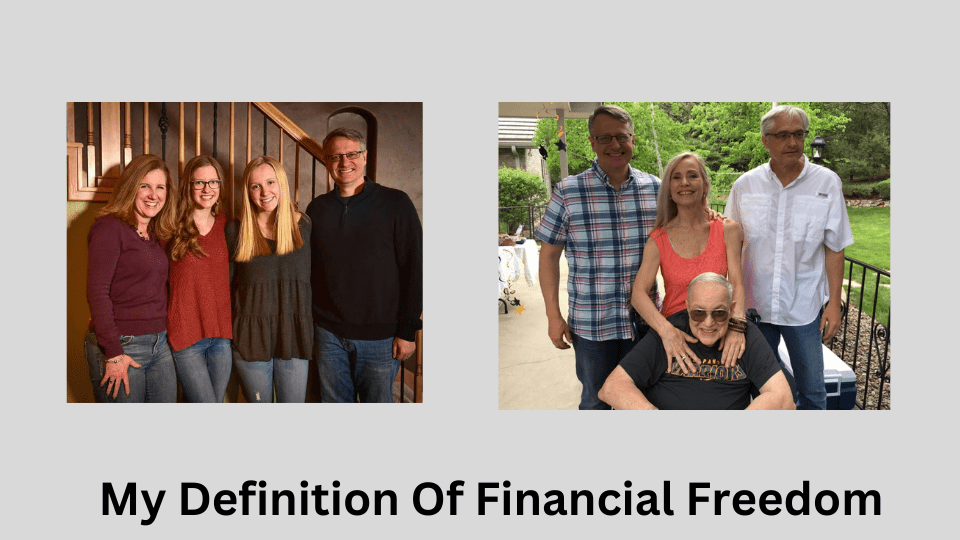

Technical definitions aside, I think a starting great framework on how to think of this is and a far better way to look at it (before we get into strict definitions) “what does financial freedom mean to you?”. Does it mean being able to retire and quit work, hanging out at the beach all day? Or does it mean having the freedom to do what you want, with whoever you want and when you want? In the end, what you hope to achieve should be the first question you ask yourself. Your own personal path will largely be determined by what your own financial freedom goal is. My own mentors at Cashflow Tactics posed this question to me when I first started on the journey to financial freedom. Honestly I really didn’t think that much of it at the time, but it’s a super important question. My own definition of financial freedom is really a two part answer: Part One: Having the ability to give my own time and support for my family. Providing mental and emotional support for my own siblings and father. Part Two: Having the freedom of choice and giving me the possibility of growing spiritually, emotionally and mentally. It’s such a squishy concept, but can be summed up in the two images below.

What Should You Think Of Before Financial Freedom?

One of the key essences of financial freedom is understanding you need to learn how to manage your money. When you choose to follow the path if financial freedom, you are taking active control of your own finances. The first step is to become more conscious of your spending habits. Make sure to account for every single paycheck. This will allow you to know how much you spend on different categories each month. You should also create a budget with room for savings and investments. This is the key to financial freedom. You may find it difficult to save a small amount of money each month, but it’s important to stay conscious of how you’re spending. For those who have a lot of debt, paying off debt is an essential component in achieving financial freedom. Many people, for example, have made their finances more secure by putting money aside for emergencies. In addition to putting money into savings, paying off debt is an important step toward creating a secure future. By saving for retirement, you’ll have more time to pursue your passions and live a life with more confidence. After an initial emergency fund is established, the bulk of your savings should go towards paying what I’ll refer as revolving debt. Personally we chose to pay down our debt so it wouldn’t be a burden on us in our own path to financial freedom. What about you, the reader? What is your own preferred path to financial freedom and how far along it are you?

Frequently Asked Questions (FAQs)

Q: What does financial freedom mean to the average person? A: Financial freedom means having enough savings, investments, or income from assets to live on your terms without worrying about day-to-day expenses or financial obligations. This could involve traveling the world, caring for a family, or living comfortably without financial constraints. Q: How can I achieve financial freedom? A: Achieving financial freedom requires several vital steps. First, You are paying off high-interest debt to eliminate financial obligations and creating and managing a budget to understand and control your income and expenses. Building an emergency fund is also essential to prepare for unexpected financial situations. Lastly, investing wisely for wealth growth and generating passive income can help you reach financial independence. Q: How can I maintain financial freedom once I’ve achieved it? A: Maintaining financial freedom involves adopting the right mindset toward spending and saving, utilizing budgeting tools and resources, protecting your assets, and planning your estate. It’s essential to continue living within your means, keep track of your finances, diversify your investment portfolio, and ensure your loved ones are cared for after your death.