Bonus Material: Click here to get the full financial freedom calculator that will calculate your returns to retire in 10 years or less - Just Make a Copy

In this article, I’m going to show you how you can determine exactly when you can retire based on your current income, annual savings, and current total savings, all using a free calculator, which I’ll refer to as the financial freedom calculator.

After you are done reading this post and using the calculator, you will know exactly what age you will be able to retire using your current saving strategy. More importantly you will know if you need to adjust your savings plan in order to meet your financial or retirement goals.

When I first went through this exercise I was SHOCKED to find out I wouldn’t be able to retire until I was 85.1 years old!

How To Use The Financial Freedom Calculator

What the calculator is about and what it will give you?

The core purpose of this calculator is to let you know exactly if your financial freedom / financial independence / retirement plan is going to work. After a series of inputs, and using some common financial assumptions it will tell you at what age you are going to be able to retire at given the current plan you are working on.

It is of course meant to be a guide and not the absolute truth. If you haven’t spent any time thinking about what financial freedom is and what it means to you, I think you should do so.

I’ve found that there is alot of “traditional” advice, such as “save 10%” or “start young” or “25x your expenses” which is just so incredibly non-specific that it won’t work.

I’ll refer to this as goldfish advice from financial advisors or “talking heads” on the internet or social media that just aren’t workable when you put pen to paper and run your actual numbers. They just regurgitate commonly held financial thoughts without actually applying any numbers to it.

Goldfish ONLY know what is in their own little fishbowl and can’t see outside of the water they have been living in for years.

At the end, you’ll get an age at which you’ll be able to retire based on your current situation. I’ll be honest, the first time I used the calculator, I was shocked to learn I wouldn’t retire until I was going to be 85!

Click the button below to make a copy of the calculator to use yourself.

Click Here To Get Your Own Copy Of The Financial Freedom Calculator

Click > Make A Copy

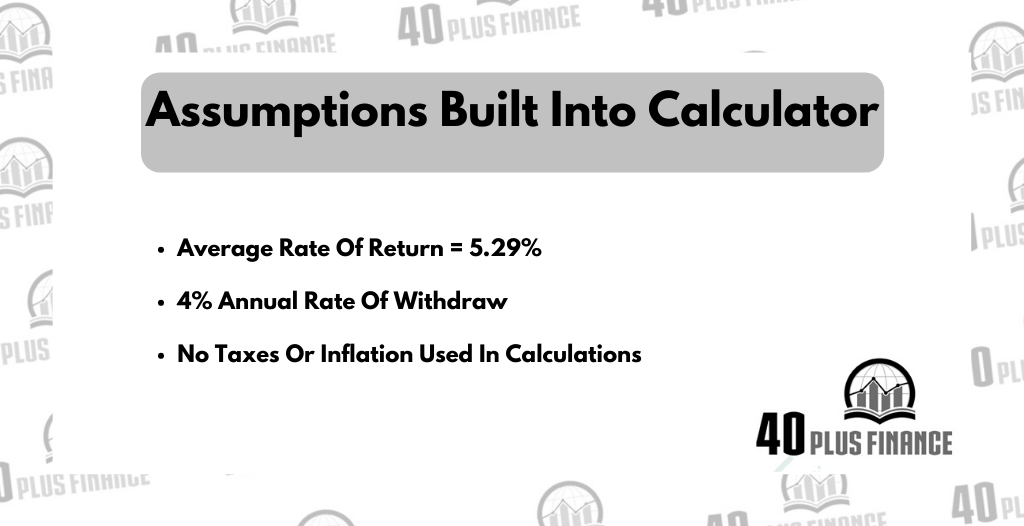

Assumptions Built Into The Financial Freedom Calculator

There are three main assumptions built into the calculator.

First is the average annual rate of return of 5.29%. This is based on a 2018 study titled “Dalbar Quantitative Analysis Of Investor Behavior” and is referenced in the calculator itself.

When you use the calculator you can use whatever number you’d like. Increase the number at your own peril.

The second assumption is that of a 4% withdrawal rate annually once you are ready to retire or want to be financially free. This is based upon research done by Wade Pfau, PhD and CFA and this research is cited in the calculator as well.

The third assumption is what we didn’t include was taxes and inflation into the calculator. Those are simply too hard to gauge and based on many many factors. This is one of the primary reasons we use income here vs expenses in the calculator. Keep this in mind!

Step 1: Provide Inputs Into The Financial Freedom Calculator

Here are the inputs or fields you will need to supply in order to make the calculator applicable for your situation:

Age - Pretty self explanatory, type your age into the required cell.

Annual Savings Amount - This is the dollar amount that you annually put towards your financial freedom/retirement goals. In the example given on the calculator, I used the standard 10% of gross current income. However, you need to input your own number based on your own situation.

Current Assets- This is the current amount of assets currently saved up. These could be in a 401k or IRA or Mutual fund. You just need to total them up and input the total into the required cell

Current Income - Put your overall gross income into this cell. This is used to determine what your “goal” is for accumulating assets based upon the 4% rule referenced above in the assumptions section. I recommend income here since there are so many variables to the calculation, including healthcare costs, rising lifestyle levels, additional taxes increases, etc. Put whatever number you feel comfortable with.

Step 2: Review Outputs From the Financial Freedom Calculator

Bonus Material: Get your copy of the full calculator that will calculate your returns to retire in 10 years or less - Just make a copy

Required Retirement Assets - This is the gross total of assets you will need to accumulate in order to meet your retirement goals, and is based upon the 4% rule for withdrawals.

Age You Can Retire - This is the age that you can actually retire based on the inputs. From this you can analyze if you current financial plan will get you to your retirement goals at the age you are aiming for.

Step 3 : Interpret Your Results

There are generally one of two ways to interpret your results:

#1) The resulting age is exactly what you have planned, or even younger. For example, if your plan calls for you to retire at 65, and the age that the calculator

So now that you have your results from the calculator, this begs the question, especially for those of us over 40, what if your age calculated is far too old?

What if you need to compress your time to retirement into 10 years or less, like alot of us need to for a full financial freedom plan?

That is why we designed the bonus calculator titled, “The Math Is The Path Tool” and it will give you your required rate of return in order to achieve financial freedom in 10 years (or whatever your number is) or less.

Bonus Materiel: Click here to get the full calculator that will calculate your returns to retire in 10 years or less. Just make a copy

Final thoughts

The financial freedom calculator is just one tool, but an extremely important one in that it can really clarify if you are on track or not for a traditional retirement or not.

Admittedly it was at first a bit shocking to see that I wasn’t on track to retire until I was 85 years old.

However, the big, important thing is that I took action on that information, took ownership of my own finances and changed the entire trajectory of my financial plan.

It is always much better to know than not know the truth about how you are tracking with your financial goals and if you need to make adjustments or not.

What about you? Are you on track or off track for financial freedom? Let us know in the comments.

Frequently Askes Questions:

Q: What is the Financial Freedom Calculator and what does it calculate?

A: The Financial Freedom Calculator is a free tool that helps determine the age you can retire based on your current income, annual savings, and total savings. By inputting these values into the calculator, you will be able to understand if your current saving strategy is sufficient to meet your financial or retirement goals and if any adjustments need to be made.

Q: What assumptions are built into the Financial Freedom Calculator?

A: The Calculator is based on three main assumptions. The first is an average annual rate of return of 5.29%, based on a 2018 “Dalbar Quantitative Analysis Of Investor Behavior” study. The second is a 4% annual withdrawal rate once you’re ready to retire. The third assumption is that taxes and inflation are not included in the calculator due to the complexity of these factors.

Q: How can I interpret the results from the Financial Freedom Calculator?

A: The results will give you an age at which you’ll be able to retire based on your current situation and inputs. If the age calculated aligns with your retirement plans, you’re on track. If the retirement age calculated is too old, it suggests that you may need to adjust your financial plans to be able to retire sooner.