What are some tips for tax efficient investing? This article will explore some concepts behind this and get you on the road to saving more in taxes.

One thing to remember is that you shouldn’t let taxes be the only factor in your investment decisions, but considering which asset classes to choose and in which accounts to hold them could help you save on taxes.

Although tax rules and rates may fluctuate over time, it is still crucial to consider taxes when making investment decisions. The reason? The amount of taxes you pay on your investment returns can vary from year to year, which could impact your ability to reach your long-term financial goals.

Before you decide on the asset class percentages that make the most sense for you, it’s helpful to understand how the IRS treats the income from those asset classes. If you earn money from interest payments on bonds or cash, the government taxes you at a rate of up to 37%, plus an additional 3.8% if the net investment income tax applies. If you have made a profit from selling stocks that you have held for more than a year, this is considered a long-term capital gain. The current tax rate for long-term capital gains is 20%, plus an additional 3.8% net investment income tax. Your gains from selling a stock will be taxed at your ordinary income rate if you held the stock for one year or less, which could be considerably higher than the capital gains rate. The following should be noted: future changes in tax law are always possible. In addition, state and local taxes may also apply.

If you are in a high tax bracket, you may want to consider how taxes will affect your investments before making any changes. It is important to speak to a professional tax advisor before making any decisions that could alter your tax situation.

Taxable Vs. Tax-Advantaged Accounts

There are two types of investment accounts: those that are subject to taxation and those that offer tax advantages.

1. Taxable Accounts

Taxable accounts do not have any tax advantages. This means that you will have to pay taxes on any money that you make from investing in capital assets. You will also receive a tax bill for any qualified dividends and interest income you have earned.

For example, a brokerage account is a taxable account. This account allows you to directly invest in stocks, municipal bonds, index funds, exchange-traded funds (ETFs), mutual funds, and real estate investments.

Brokerage accounts are flexible, as they are generally liquid. However, you will have to pay taxes on the money you make in this account when you cause a taxable event (for example, selling stock for a profit).

When you have a brokerage account, it is important to take note of how long you keep your investments. If you make a profit from trading a stock within 12 months, you will have to pay a short-term capital gains tax based on your ordinary income tax bracket.

If you hold an investment for more than one year, you will not have to pay taxes on any profit you make, you will pay taxes on 15% of the profit you make, or you will pay taxes on 20% of the profit you make. The amount of money you owe in taxes on your capital gains will depend on which tax bracket you fall into.

2. Tax-advantaged Accounts

Tax-advantaged accounts still require you to pay taxes. Although they make you wait longer to get your money, they let you have more control over when you pay taxes. Do your research to see what account types are available to you and what the different features are between them.

Tax-exempt Accounts

You can contribute after-tax dollars to fund your retirement with tax-exempt accounts like Roth IRAs and Roth 401(k)s. This means that you won’t get a tax break when you use either of these Roth accounts.

The tradeoff is that you will not have to pay taxes on your investments until you reach retirement age. You won’t have to pay taxes on your required minimum distributions during retirement.

Tax-deferred Accounts

With tax-deferred accounts, you don’t pay taxes on the money you contribute upfront. Instead, you pay taxes later when you withdraw the money during retirement. If you have this type of account, you can deduct it from your taxes, which will lower the amount you owe. This means that you’ll have to pay taxes when you start to use the money you saved for retirement. The advantage is that you will have more money to increase your wealth over time, while reducing your income tax rate in the short term.

7 Tax-Smart Tips For Investors

Here are some ways to reduce what you owe in taxes.

1. Maximize tax-deferred retirement accounts.

There’s nothing wrong with opening a brokerage account. An investor may do this in order to have funds for short-term to medium-term savings.

You might open a brokerage account if you want to save money for a big purchase, like a car or a house. An account with a broker can help you earn more money than you would by just keeping your cash in a savings account.

As an investor, you need to think about the long-term future, not just the next five or 10 years. It is important to save as much money as possible for retirement so that you can take care of yourself in the future. You can reduce the amount of money you have to pay in taxes by investing in a 401(k) or IRA.

How contribution limits work:

There are limitations on how much you can contribute to a tax-advantaged account.

For example, you can contribute a maximum of $20,500 to a 401(k) account in 2023 without facing a penalty. In addition to any money your employer might put in your account,

Roth and traditional IRAs have much lower contribution limits of $6,000. You cannot contribute more than $6,000 in total to both a Roth IRA and a traditional IRA.

If you are self employed, you may be able to contribute up to $61,000 to a Simplified Employee Pension (SEP) IRA for the 2022 tax year.

If you are eligible for a 401(k) through work, you should open an account and start contributing to it as soon as possible. Along with this, you should also open an IRA on the side. The best way to save for retirement is to focus on maxing out your 401(k) and putting additional income into your IRA.

2. Diversify your account types.

A mix of investment account types can help you minimize your taxes in retirement by matching income sources.

Different investment account types offer different tax treatments.

- Traditional IRAs and pre-tax 401(k) contributions offer federal tax-deferred growth potential.

- Roth IRAs and Roth 401(k) contributions offer the potential for growth that won’t be federally taxed if account owners meet requirements for qualified distributions (state taxes may apply).

- Brokerage accounts offer taxable growth potential.

Here are some examples of how diversifying can benefit your investments:

- If you are eligible to take tax deductions in retirement, you’ll need taxable income in order to take advantage of them. Withdrawals from a traditional IRA or pre-tax 401(k) count as taxable income, so you could withdraw only enough to offset your eligible deductions and then draw the rest from your Roth account. Qualified distributions from Roth accounts are federally tax-free (and may be state-tax-free).

If you have taxable accounts that you can draw from during retirement, you can allow your traditional IRA and pre-tax 401(k) assets to continue growing without having to pay taxes on them until you reach the required beginning date, after which time you must take minimum distributions.

- Money contributed to a traditional IRA or 401(k) on a tax-deductible or pre-tax basis is taxed upon withdrawal at your future tax rate, which may be lower than your current rate. In contrast, money contributed to a Roth IRA or Roth account 401(k) plan is taxed at current federal rates, and qualified distributions are federally tax-free and also may be exempt from state tax.

Diversifying your accounts may help reduce your taxes in retirement. Planning ahead by establishing different types of accounts can help you take advantage of lower tax rates in the future. It is often a good idea to keep as much money as possible in your retirement accounts for as long as possible so that the money can keep growing without being taxed. The required minimum distribution is the minimum amount of money that must be withdrawn from a retirement account each year. As long as you’re still working, you’re not required to take a minimum distribution from your non-Roth qualified retirement plan accounts. If you have an IRA as your retirement plan account, you must start taking RMDs by the required age, even if you are still employed.

3. Choose tax-efficient investments.

Specific investments can carry tax benefits, as well. For example, income earned from municipal bonds is not taxed at the federal level, and in some cases, it is not taxed at the state or local level either. The income from tax-exempt bonds is exempt from taxes when it is held directly, but when it is distributed from a retirement account, it is considered ordinary income and is taxed.

Investments that take taxes into account may include tax-managed mutual funds, whose managers strive for tax efficiency, as well as index funds and exchange-traded funds that mirror long-term investments in a target index. Before investing in municipal bonds, it is important to speak with a tax advisor to ensure you understand the tax implications of these investments. Additionally, you should determine whether the lower yield of municipal bonds makes them a worthwhile investment for your non-retirement account portfolio.

4. Match investments with the right account type.

You should hold your tax-efficient investments in accounts with the best possible tax treatment. This type of investment can help you get the most out of tax benefits without raising your taxes.

If you have investments that generate taxable income, it may be better to hold them in a tax-deferred account like a traditional IRA in order to get the best possible tax benefit. Withdrawals you take during retirement from a Roth account may not be taxed at all. Withdrawals from other accounts may be taxed at your ordinary income rate, which may be lower at that time.

Tax-neutral investments are those that neither generate taxable income nor provide a tax deduction, making them ideal for a taxable brokerage account where taxes are not deferred. The reason? If your investments don’t result in high taxes, you don’t need to defer them, so there is no reason to put them in an account that could restrict your access to them. It is important to ensure that the investment choices you make are in line with your wider financial goals.

5. Hold investments longer to avoid unnecessary capital gains.

It is not worth it to keep a stock you are ready to sell just to avoid taxes, except for one instance. While stocks held for a year or less result in gains that are taxed at federal ordinary income rates, stocks held for longer than a year result in gains that are taxed at the federal long-term capital gains rate. The long-term capital gains rate is currently 15% for most investors and 20% for high-income taxpayers, plus the potential 3.8% net investment income tax. It may make sense to postpone selling stocks that have increased in value so that they can be sold as long-term capital gains. Again, always check with your tax advisors.

6. Look into tax-loss harvesting.

You should look into reducing taxes for a brokerage account in addition to maximizing tax-advantaged accounts. This is possible through a strategy called tax-loss harvesting.

What is tax-loss harvesting?

A tax-loss harvesting strategy can help reduce the amount of taxes you owe by using investment losses to offset capital gains taxes or up to $3,000 of ordinary income if you’re married and filing jointly.

The IRS does not allow people to deduct capital losses from the sale of securities against capital gains distributions on the same security. This is called a wash sale. A write-off is allowed only if you buy the same security, an option or option to buy a security, or an identical one within 30 days before or after you sold the investment that produced a loss. If you violate the “wash sale” rule, the IRS may impose penalties.

It is beneficial to speak with a tax specialist before taking any action. It is important to look at your investment portfolio closely and decide if it would be a good idea to sell a security and get rid of it, or if it would be better to keep it in case it grows more in the future.

Investors often choose tax harvesting for investments that do not fit their strategy or have little to no growth potential or dividend yield.

7. Think about how you earn your income

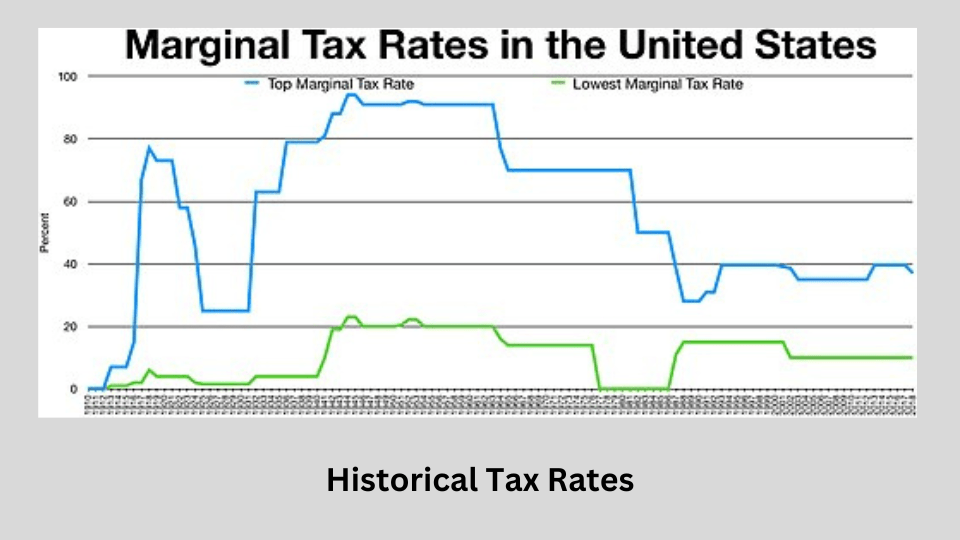

An important final concept is that different types of income are treated differently from a tax perspective. This concept was made famous by Robert Kiyosaki in his book, “Cashflow Quadrant” where he explains that the manner in which people earn their income has an enormous impact on on how much in taxes they pay. Employees, Small Businesses, Business & Investors all pay taxes in different ways. The largest chunk of taxes are paid by people who are either employees or own a small business. For example, if you earn income through real estate investments, you can use depreciation to offset any cashflow from your assets to essentially make it become tax free income. Final Thoughts One final concept here is to consider whether you’d like to pay your taxes now, or in the future. The saying goes of paying taxes on the seed rather than the harvest. Especially in todays economic environment with rampant inflation, large government bailouts and deficit spending, how to you think the government will pay for those programs? Through taxes. As you can see from the graph below, we are in a historically low tax rate environment.  Image Source = WikiMedia. “Marginal Tax Rates In The United States, https://commons.wikimedia.org/w/index.php?title=File:Historical\_Marginal\_Tax\_Rate\_for\_Highest\_and\_Lowest\_Income\_Earners.jpg&oldid=501930427” Taxes certainly won’t go much lower and historically are much higher. You could consider paying taxes on an investment now with the amount being a known quantity vs. an unknown amount in the future.

Image Source = WikiMedia. “Marginal Tax Rates In The United States, https://commons.wikimedia.org/w/index.php?title=File:Historical\_Marginal\_Tax\_Rate\_for\_Highest\_and\_Lowest\_Income\_Earners.jpg&oldid=501930427” Taxes certainly won’t go much lower and historically are much higher. You could consider paying taxes on an investment now with the amount being a known quantity vs. an unknown amount in the future.

{kind=link}

Finally, You need to be aware of the tax implications of your investment choices regardless of how you choose to invest your money. It is important to keep track of what you owe throughout the year and to use the tips above to reduce your tax burden. And don’t hesitate to hire a qualified tax advisor.

If you carefully consider how to minimize your taxes when investing, you could save a lot of money on taxes at the end of the year.

This is how you can create a stronger, more diversified portfolio that will help you achieve financial freedom.