Have you ever paused to think about how much it truly costs to receive long-term care? As people live longer and healthcare advances, the demand for long-term care is skyrocketing. This surge is impacting financial plans and reshaping how we approach future needs.  Understanding the rising costs is crucial if you aim to secure your financial future and care needs. By exploring these ten facts, you’ll grasp the challenges and consider potential solutions to prepare for what lies ahead.

Understanding the rising costs is crucial if you aim to secure your financial future and care needs. By exploring these ten facts, you’ll grasp the challenges and consider potential solutions to prepare for what lies ahead.

1) Long-term care costs have outpaced inflation rates.

Have you ever wondered why the cost of long-term care seems to rise faster than inflation? It’s a real concern for many of us. Long-term care costs are climbing at a rate that outpaces what’s happening with inflation. This means even if you’re saving diligently, your money might not stretch as far as needed. Think about this: according to the Genworth 2019 Cost of Care Survey, the expenses for long-term care are increasing more quickly than inflation. This trend can make it tough for individuals to plan for the future, impacting financial security. What does this mean for you and your family? The Genworth 2023 Cost of Care Survey offers insights into why these costs are rising. Factors such as increased demand for services, workforce shortages, and higher operating costs all play a role. If you’re not prepared, these costs could eat into your savings faster than you expect. Now, let’s consider this: 70% of seniors might require some form of long-term care at some point in their lives. That’s a staggering number, implying a significant need for services that keep getting more expensive. Are you ready for this possibility? This isn’t just about nursing homes. Whether it’s home health care, assisted living, or skilled nursing, the financial implications are serious. With home health costs projected to double from 2019 to 2030, as reported by Forbes, it’s clear that the financial landscape is shifting. Looking ahead, what’s the strategy? It’s critical to consider how these rising costs will fit into your long-term financial plans. Are we truly prepared to tackle this challenge head-on? It might be time to rethink traditional approaches and explore options that align better with these new realities.

2) Nursing home prices have risen over 40% in the last decade.

When I look at the numbers, I see a clear picture: nursing home costs have skyrocketed. Over the last ten years, prices for nursing home care have increased by more than 40%. This kind of rise can catch many off guard. Are you prepared for these costs in your retirement plan? Imagine what your money would have looked like a decade ago. The average cost for a private room in a nursing home was significantly lower, around $77,745 back in 2011. By 2021, it reached about $108,405, up nearly 40%. That’s quite a jump for anyone planning their future finances. This increase isn’t just a number on a page. It affects real people and families. Those of us planning for the future have to think carefully about how these rising costs fit into our financial plans. Have you considered how this might impact your savings or retirement goals? These rising costs aren’t gliding upward without reason. Factors like increased demand for skilled nursing care and higher operation costs at healthcare facilities contribute to this surge. And given that a significant number of people will need some form of long-term care, these trends can seem daunting. Are you starting to feel the need to reassess your financial strategies? Thinking about long-term care costs should be an essential part of your retirement planning. Would you be ready to handle such increases on your current savings plan? Preparing now could save stress down the road.

3) Home Health Aide Expenses Increased by an Average of 2.9% Annually

Have you ever thought about how quickly expenses add up when it comes to home care? It’s astonishing. Home health aide costs have been climbing at an average rate of 2.9% per year. This isn’t just a statistic—it’s a real impact on your wallet and plans for the future. Why is this happening? As the demand for home health care grows, so do labor costs. More people need care as they age, leading to increased demand for skilled aides. This rising demand pushes wages up, making services more expensive. Imagine balancing these costs while saving for retirement or supporting your kids. This can feel daunting, especially when inflation eats away at your savings. Have you considered how provisions for health care will affect long-term financial plans? Many families aim to keep elderly relatives at home for comfort and familiarity. Home health care provides a solution, but there’s no denying the financial strain it can create. Are you prepared to make the necessary adjustments to accommodate these costs? Finding alternatives to manage growing expenses is crucial. From insurance options to financial planning, there are paths to explore. Don’t be caught off guard by rising expenses. Taking proactive steps now can alleviate stress later and safeguard your financial security. Planning for home health care is a vital component of sound financial health. Are you taking the necessary steps to ensure you’re ready for the unexpected challenges that lie ahead?

4) Assisted living facility costs are expected to double by 2040.

Have you noticed how everything seems to be getting more expensive? It’s not just your imagination. Assisted living costs are on the rise. By 2040, these costs are expected to double. That’s a big jump for anyone planning for future care. Why is this happening? One reason is the demand for quality care. As more people require assisted living, facilities invest in better services and staff. This, of course, raises the price. Are you ready to face those costs when the time comes? In the past, assisted living wasn’t as expensive. Today, though, it’s a different story. Imagine paying twice the amount you’re planning for now. It makes me wonder how prepared I really am for my later years. So, what can we do about it? It’s essential to plan ahead and consider options like insurance or savings. Do you have a financial strategy in place? Preparing today might be the difference in affording the care you or your loved ones need tomorrow. The rising costs are not just a warning; they’re a call to action. Ensuring you have a solid plan means you won’t be caught off guard when prices surge. Can you really afford to wait and see with your future on the line?

5) Medicare doesn’t cover most long-term care expenses.

Did you know that Medicare doesn’t cover most long-term care expenses? These costs can put a massive dent in anyone’s savings. Many assume all healthcare needs will be met once they hit 65, but that’s not the full story. Medicare does provide for short-term care within skilled nursing facilities, usually after a hospital stay. This is crucial but only covers a small part of long-term needs. Skilled nursing is different from custodial care, which involves help with daily activities like bathing or eating. Long-term custodial care is typically not part of Medicare coverage. This means individuals might face out-of-pocket expenses for services many eventually need as they age. Have you considered how this could impact your financial plans? Medicare does cover some other aspects, such as hospice care, which supports end-of-life needs. It also pays for some home healthcare services when they’re deemed medically necessary. Yet, most long-term care costs fall outside these benefits. It’s vital to understand your options. Could long-term care insurance be a part of your strategy? Or might Medicaid provide a safety net for those with limited resources? Start exploring these avenues now before it’s too late. How ready are you for the unexpected? Having a strategy for long-term care expenses could be the key to protecting your hard-earned savings. The sooner you plan, the more secure your financial future might become.

Did you know that Medicare doesn’t cover most long-term care expenses? These costs can put a massive dent in anyone’s savings. Many assume all healthcare needs will be met once they hit 65, but that’s not the full story. Medicare does provide for short-term care within skilled nursing facilities, usually after a hospital stay. This is crucial but only covers a small part of long-term needs. Skilled nursing is different from custodial care, which involves help with daily activities like bathing or eating. Long-term custodial care is typically not part of Medicare coverage. This means individuals might face out-of-pocket expenses for services many eventually need as they age. Have you considered how this could impact your financial plans? Medicare does cover some other aspects, such as hospice care, which supports end-of-life needs. It also pays for some home healthcare services when they’re deemed medically necessary. Yet, most long-term care costs fall outside these benefits. It’s vital to understand your options. Could long-term care insurance be a part of your strategy? Or might Medicaid provide a safety net for those with limited resources? Start exploring these avenues now before it’s too late. How ready are you for the unexpected? Having a strategy for long-term care expenses could be the key to protecting your hard-earned savings. The sooner you plan, the more secure your financial future might become.

6) The median annual cost for a private room in a nursing home is over $100,000.

Have you ever thought about the real cost of aging? A significant figure looms: the median annual cost for a private room in a nursing home is over $100,000. This is not just a number; it’s a stark reality that many of us might face. Imagine paying that much every year. It’s like buying a new car annually, but instead, it’s for a single room. When thinking about retirement, these costs should factor heavily into your planning. Why does it cost so much? It’s not just about the room itself. It’s about the level of care provided. Private rooms offer more privacy and personalized care. Yet, this comfort comes with a hefty price tag. Does this mean we need to save more, invest differently, or reassess our financial goals? Possibly. This high cost of care can eat into savings quickly, which means relying solely on traditional saving methods might leave you unprepared. Some states have varying costs based on location. For instance, Genworth reports that prices differ across the country. Knowing these regional differences can be crucial when planning where to retire or where your loved ones might need care. Have you ever wondered if long-term care insurance could help? It’s worth considering. While it may not cover all expenses, it could mitigate some financial burdens. Facing the costs of long-term care requires clear thinking and strategic planning. Taking action before it becomes a necessity can make all the difference.

Have you ever thought about the real cost of aging? A significant figure looms: the median annual cost for a private room in a nursing home is over $100,000. This is not just a number; it’s a stark reality that many of us might face. Imagine paying that much every year. It’s like buying a new car annually, but instead, it’s for a single room. When thinking about retirement, these costs should factor heavily into your planning. Why does it cost so much? It’s not just about the room itself. It’s about the level of care provided. Private rooms offer more privacy and personalized care. Yet, this comfort comes with a hefty price tag. Does this mean we need to save more, invest differently, or reassess our financial goals? Possibly. This high cost of care can eat into savings quickly, which means relying solely on traditional saving methods might leave you unprepared. Some states have varying costs based on location. For instance, Genworth reports that prices differ across the country. Knowing these regional differences can be crucial when planning where to retire or where your loved ones might need care. Have you ever wondered if long-term care insurance could help? It’s worth considering. While it may not cover all expenses, it could mitigate some financial burdens. Facing the costs of long-term care requires clear thinking and strategic planning. Taking action before it becomes a necessity can make all the difference.

7) Adult Day Health Care Services Are a More Affordable Option

When thinking about long-term care, the first thing that often comes to mind is cost. It’s understandable. Who wouldn’t want an option that doesn’t break the bank? That’s where adult day health care services shine. These services offer a structured setting during the daytime for seniors. They provide not just supervision, but also social interaction and health-related services. In comparison to other long-term care services, this can be much easier on the wallet. Consider the typical expenses associated with nursing homes. For many, these costs are overwhelming and can quickly deplete savings. But adult day care, with costs ranging from as low as $25 to over $100 a day, provides a much-needed respite for both the caregiver and the family budget. Imagine being able to go about your day knowing your loved one is in capable hands—without the astronomical costs. It feels almost liberating. Plus, some insurance plans can help cover these expenses, further easing the financial burden. What about the daily interaction and care your loved ones receive? Adult day care centers often provide activities, meals, and even medical services tailored to meet individual needs. This can enhance the quality of life for seniors while keeping costs in check. So, why not consider adult day health care? It’s a practical and affordable choice for those looking to manage long-term care expenses wisely. By opting for these services, you maintain both financial health and peace of mind—key elements in any solid financial strategy.

When thinking about long-term care, the first thing that often comes to mind is cost. It’s understandable. Who wouldn’t want an option that doesn’t break the bank? That’s where adult day health care services shine. These services offer a structured setting during the daytime for seniors. They provide not just supervision, but also social interaction and health-related services. In comparison to other long-term care services, this can be much easier on the wallet. Consider the typical expenses associated with nursing homes. For many, these costs are overwhelming and can quickly deplete savings. But adult day care, with costs ranging from as low as $25 to over $100 a day, provides a much-needed respite for both the caregiver and the family budget. Imagine being able to go about your day knowing your loved one is in capable hands—without the astronomical costs. It feels almost liberating. Plus, some insurance plans can help cover these expenses, further easing the financial burden. What about the daily interaction and care your loved ones receive? Adult day care centers often provide activities, meals, and even medical services tailored to meet individual needs. This can enhance the quality of life for seniors while keeping costs in check. So, why not consider adult day health care? It’s a practical and affordable choice for those looking to manage long-term care expenses wisely. By opting for these services, you maintain both financial health and peace of mind—key elements in any solid financial strategy.

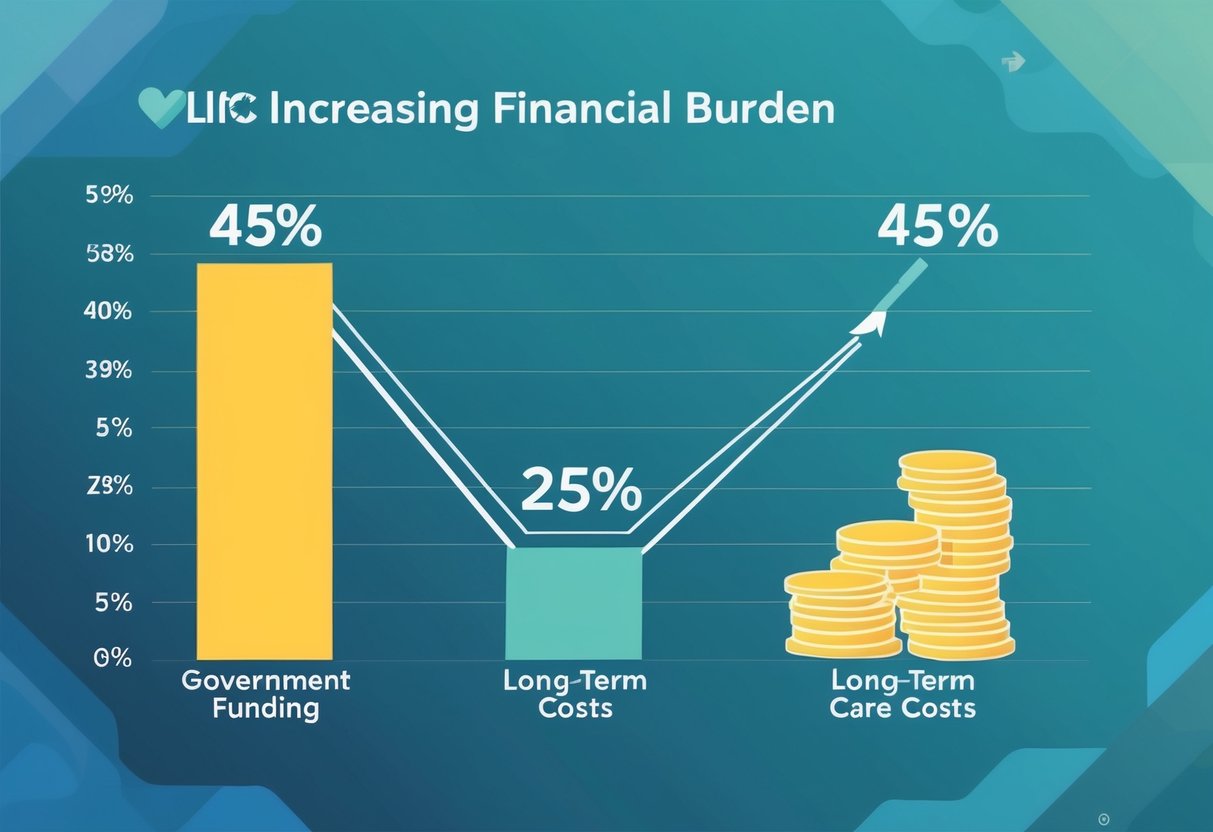

8) Government funding covers only about 45% of national long-term care costs

Did you know government funding handles just 45% of long-term care expenses in the U.S.? It’s a surprising fact for many who assumed it would cover more. You might wonder, “Who covers the rest?” The answer is individuals, either out of their pockets or through private insurance. Many people mistakenly believe Medicare will cover long-term care, but it’s actually Medicaid that steps in. And, Medicaid primarily serves those with limited income. How many have thought about this crucial gap? Not enough, if you ask me. This reality can shake your confidence in retirement plans. With only part of these costs covered by the government, it’s crucial to plan for the future. Many folks, especially those in their 40s and 50s, are blindsided when they realize how expensive long-term care can be. This is where the real challenge lies for many working adults with families to support. Being prepared financially for long-term care is essential. We all want to ensure our families are taken care of without depleting savings. Have you considered the importance of setting aside funds specifically for long-term care? If not, now is the time to start thinking about it. It might seem daunting, but understanding the limitations of government coverage can be empowering. Once you know what’s at stake, you can make more informed decisions for your future. Consider consulting with a financial advisor to carve out a solid plan that suits your needs.

Did you know government funding handles just 45% of long-term care expenses in the U.S.? It’s a surprising fact for many who assumed it would cover more. You might wonder, “Who covers the rest?” The answer is individuals, either out of their pockets or through private insurance. Many people mistakenly believe Medicare will cover long-term care, but it’s actually Medicaid that steps in. And, Medicaid primarily serves those with limited income. How many have thought about this crucial gap? Not enough, if you ask me. This reality can shake your confidence in retirement plans. With only part of these costs covered by the government, it’s crucial to plan for the future. Many folks, especially those in their 40s and 50s, are blindsided when they realize how expensive long-term care can be. This is where the real challenge lies for many working adults with families to support. Being prepared financially for long-term care is essential. We all want to ensure our families are taken care of without depleting savings. Have you considered the importance of setting aside funds specifically for long-term care? If not, now is the time to start thinking about it. It might seem daunting, but understanding the limitations of government coverage can be empowering. Once you know what’s at stake, you can make more informed decisions for your future. Consider consulting with a financial advisor to carve out a solid plan that suits your needs.

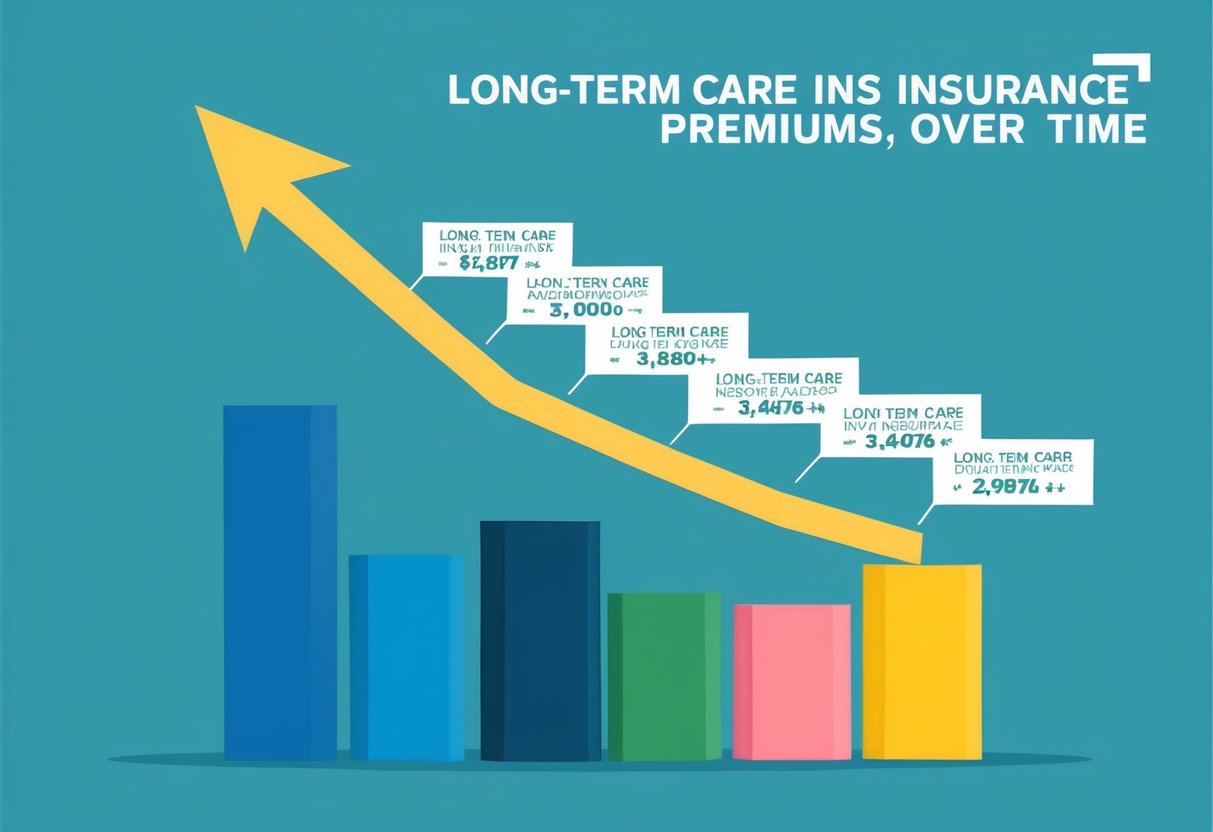

9) Private long-term care insurance premiums have surged.

Have you noticed the climb in long-term care insurance premiums? It’s been significant. Many policyholders are seeing premiums jump by substantial amounts. For a policy lasting 15 years, imagine paying $3,000 annually only to face an increase to $5,000 later on. Why is this happening? Insurance companies are adjusting their rates due to the rising costs of healthcare and longer life expectancy. They need to manage their risk and ensure they can meet future claims. This shift in pricing strategy is impacting many who had already budgeted for their retirement. Facing these increases can be frustrating. It is often challenging to decide whether to continue with higher premiums or explore other options. Inflation and changing economic factors play a role in these adjustments as well. Insurers are reevaluating how to price their services accordingly. It’s important to stay informed about your options. One strategy might be to adjust the benefits of your existing policy to lower the premiums. Another option could be shopping around for a better deal or reconsidering your long-term care needs. Understanding this trend can help you make informed choices about your financial future. If I were in this situation, I’d examine my budget carefully and think about the coverage I truly need. Is this extra financial burden worth the peace of mind? These are the questions I’d ask myself.

Have you noticed the climb in long-term care insurance premiums? It’s been significant. Many policyholders are seeing premiums jump by substantial amounts. For a policy lasting 15 years, imagine paying $3,000 annually only to face an increase to $5,000 later on. Why is this happening? Insurance companies are adjusting their rates due to the rising costs of healthcare and longer life expectancy. They need to manage their risk and ensure they can meet future claims. This shift in pricing strategy is impacting many who had already budgeted for their retirement. Facing these increases can be frustrating. It is often challenging to decide whether to continue with higher premiums or explore other options. Inflation and changing economic factors play a role in these adjustments as well. Insurers are reevaluating how to price their services accordingly. It’s important to stay informed about your options. One strategy might be to adjust the benefits of your existing policy to lower the premiums. Another option could be shopping around for a better deal or reconsidering your long-term care needs. Understanding this trend can help you make informed choices about your financial future. If I were in this situation, I’d examine my budget carefully and think about the coverage I truly need. Is this extra financial burden worth the peace of mind? These are the questions I’d ask myself.

10) About 70% of People Over 65 Will Need Long-Term Care Services.

Did you know that nearly 70% of people over the age of 65 will eventually need some form of long-term care? This statistic is eye-opening for many. It’s not just about planning for the unexpected, but realizing that this might be a reality most of us will face. Why is this important? As you reach retirement age, you want to ensure your finances are prepared for potential long-term care needs. Planning now can prevent financial strain later. Ignoring the possibility could mean unexpected expenses that eat into your savings or reduce your retirement comfort. Long-term care isn’t limited to nursing homes. It includes a range of services, from home help to assisted living. This diversity means there are options to fit different needs and preferences. It’s crucial to consider what might be the best choice for you or a loved one. How do you prepare for this? Consider looking into long-term care insurance or setting aside a portion of your investments specifically for this purpose. Being aware and taking steps now can make all the difference in maintaining your desired lifestyle. Growing older doesn’t have to mean losing control of your financial future. Stay informed, make plans, and approach the years ahead with confidence.

Did you know that nearly 70% of people over the age of 65 will eventually need some form of long-term care? This statistic is eye-opening for many. It’s not just about planning for the unexpected, but realizing that this might be a reality most of us will face. Why is this important? As you reach retirement age, you want to ensure your finances are prepared for potential long-term care needs. Planning now can prevent financial strain later. Ignoring the possibility could mean unexpected expenses that eat into your savings or reduce your retirement comfort. Long-term care isn’t limited to nursing homes. It includes a range of services, from home help to assisted living. This diversity means there are options to fit different needs and preferences. It’s crucial to consider what might be the best choice for you or a loved one. How do you prepare for this? Consider looking into long-term care insurance or setting aside a portion of your investments specifically for this purpose. Being aware and taking steps now can make all the difference in maintaining your desired lifestyle. Growing older doesn’t have to mean losing control of your financial future. Stay informed, make plans, and approach the years ahead with confidence.

Understanding the Basics of Long-Term Care Costs

Long-term care costs often surprise many with their complexity and high price tags. By exploring definitions and cost drivers, you gain insights to prepare financially for yourself and your loved ones.

Long-term care costs often surprise many with their complexity and high price tags. By exploring definitions and cost drivers, you gain insights to prepare financially for yourself and your loved ones.

Definition and Scope of Long-Term Care

Long-term care involves more than just medical help. It’s not just about hospitals or doctor visits; it’s about assistance with everyday activities. Imagine needing help with bathing, dressing, or even eating. This care can happen at home, in community centers, or specialized facilities. These services focus on providing quality of life and independence for those unable to fully care for themselves. The scope varies based on the individual’s health and daily needs. From a few hours a week to 24/7 assistance, care plans can be explicitly tailored. Understanding these needs is crucial to plan effectively for the future.

Factors Contributing to Cost Increases

What makes long-term care so expensive? First, consider the rapidly growing number of seniors. Demand for services continues to rise, pushing prices higher. Then there’s the cost of labor. Skilled caregivers and healthcare workers demand competitive wages, adding to the overall cost. In states like Alaska, care prices exceed the national average due to higher living costs and remote locations. Care levels also matter, as private nursing home rooms can cost over an average of $108,405 a year. Keeping track of these factors helps you stay ahead in managing potential financial burdens.

Economic Impact of Rising Long-Term Care Costs

Rising long-term care costs are reshaping the financial landscape. These costs affect not just those needing care but ripple through families and the healthcare system. Individuals often face tough choices, while healthcare systems grapple with increased demand and resource allocation.

Rising long-term care costs are reshaping the financial landscape. These costs affect not just those needing care but ripple through families and the healthcare system. Individuals often face tough choices, while healthcare systems grapple with increased demand and resource allocation.

Effect on Individuals and Families

How do families cope when long-term care costs skyrocket? Many find themselves caught in a financial bind. With an average annual cost of a nursing home room totaling over $94,000 in 2021, paying out of pocket can be a massive burden. Insurance might cover some costs, but there’s often still a significant gap for families to bridge. These expenses can deplete savings and force tough decisions. Do they cut other expenses, dip into retirement funds, or sell assets? What about leaving something for their children? This financial strain can rip through family budgets, often leading to debt. Families can feel pressured, making financial planning more critical than ever before. It’s not just about numbers; it’s about securing peace of mind for the future.

Implications for Healthcare Systems

The healthcare system faces its own set of challenges. As more people require assistance, the demand for skilled nursing and home care rises sharply each year. Labor costs for aides, nurses, and therapists continue to increase, straining budgets and resources. Isn’t it surprising how these costs impact the availability and quality of care? Healthcare providers are forced to juggle between offering quality services and maintaining financial sustainability. More people needing care can lead to longer wait times and reduced quality of service. These pressures require innovative solutions to balance costs and care quality, pushing for reforms that are often slow to come. The system must evolve to sustain itself in the face of growing demands.